THEORY OF DEMAND

Demand refers to quantity of the goods and services consumers are able and willing to purchase at the prevailing price in a given period of time.

According to Bober “By demand we mean the various quantities of a given commodity or service which consumers would buy in one market in a given period of time at various prices or at various incomes, or at various prices related goods.

From the point of view of the seller, the demand price is the average revenue (revenue per unit) or income he expects to earn from the sale of unit of a commodity.

Thus, demand price is identical with average revenue (AR). That is why; the demand curve is also drawn as AR curve.

The law of demand states that “The higher the price the lower the demand, the lower the price the higher the demand, other factors remaining constant.

Assumptions of the law of demand

The law of demand operates when all factors affecting demand apart from the price of the commodity are kept constant,

Therefore the following are the assumptions of the law of demand;-

<> No change in the level of distribution of income

<> The consumer’s level of income remains the same

<> Population size remains unchanged

<> The prices of other related goods remains the same

<> There is no change in taste and preferences

<> The level of advertisement remains the same

<> The level of income tax remains unchanged.

<> The Demand Schedule

This is the table that shows different price levels and the corresponding quantities demanded of the commodity

Price of milk per ltr in Tshs. | 100 | 200 | 300 | 400 |

Quantity demanded of milk in ltrs | 8 | 6 | 4 | 1 |

Types of Demand Schedule

Individual demand schedule -This is the type of table which shows different quantities demanded of the commodity by an individual

Market demand schedule– This is the table which shows different total quantities demanded of the commodity at different prices in the whole market.

NOTE. In order to get a market demand schedule we add up individual demand schedules.

Price of milk per ltr | Qty demanded milk by John in ltr | Qty demanded of milk by Jane ltrs | Market demand |

100 | 8 | 6 | 14 |

200 | 6 | 4 | 10 |

300 | 4 | 2 | 6 |

400 | 1 | 1 | 2 |

Assuming there are two buyers in the market for milk, John and Jane, the market demand schedule will be derived as above

The Demand Curve

This is a graphical presentation of the demand schedule showing the relationship between price of the commodity and its demand.

A demand curve has a negative slope and its slopes downwards from left to right showing that as the price decrease the quantity demanded increases, other factors remaining constant.

The demand curve

The demand curve of Jane

FACTORS AFFECTING DEMAND

Demand of a good or service will be high or low depending on the following factors;-

1. The price of the commodity.

When the price of the commodity is high the demand will be low, and when the price of low demand will be high, other things being constant.

2. Population size

The demand on an area with high population will be high while the demand of the area with low population will be low.

3. Consumer’s level of income

When the consumer’s level of income is high, the demand will be high as the consumer’s ability will be high.

However the consumer’s level of income is low, the demand will also be low as the consumer’s ability will be low.

4. Level of advertisement

The commodity which is extensively advertised will be highly demanded, while the commodity which is not advertised the demand will be low.

5. Tastes and Preference.

If the commodity is favored, people’s taste and preference, the demand will be high while the commodity which is not favored by people’s tastes and preference the demand will be low.

E.g. the demand of Hi-jab in Saudi Arabia is higher compared to the demand in USA.

6. The level of Taxation.

When the income tax charged is high, demand will be low and when the income tax is low, demand will be high, in which the disposable personal income will be high.

7. The price of the substitute goods

If the price of the substitute increases demand of the good will decrease and when the price of the substitute decreases the demand of good in qn will increase.

Substitutes are goods for which one can be used instead of the other e.g. pepsicola and Coca-Cola

Price of the complement

Complement goods which are jointly demanded. These are goods which the demand of one result into demand of the other e.g. Car & petrol.

If the price of the complement is high the demand of the good in question will be low and when the price of the complement is low the demand f the good in question will be high. (e.g. When the price of a car is high, demand for petrol will be low and when the price of the car is low, demand for petrol will be high)

Season

The demand of some goods is seasonal in nature. When the prevailing seasons favors certain goods, its demand will be high and when the prevailing season does not favor a certain good, its demand will be low.

E.g. The demand of woolen jacket in winter will be high compared to the demand of woolen jacket in summer which will be low.

The downward sloping demand curve

The demand curve slopes downwards from left to right (negative slope). The indicates that more is demanded as the price falls and less is demanded when the price increases such negative slope is due to the following factors;-

Income effect

As the price falls real income, increases and therefore consumers can now buy more units of a commodity with the same income. On the other hand when the price increases, real income decrease and therefore consumers can now buy less units with the same income.

2. The law of diminishing marginal utility.

The law of diminishing marginal utility states that,” as more and more units of the commodity is consumed the additional satisfaction goes on declining” therefore more and more units of the commodity will be purchased only if the price is falling.

3. Substitution effect.

When the price of the commodity is low it becomes cheaper in comparison to other competing commodities and the consumers start to substitute this commodity in place of other commodity therefore demand for the commodity increases with the fall in price

4. New customers

When the price of the commodity for new customers join buying that commodity those who could not afford before and hence increase in demand, on the other hand when the price rises, some old customers may stop to purchase the commodity and hence fall in demand.

Uses of the commodity.

A commodity tends to be to more uses or less urgent uses when it becomes cheaper. For example, if water is dear, we shall use it for drinking only, but when it becomes cheaper, we shall use it for washing and other less urgent uses.

Change in quantity demanded and change in demand

Change in quantity demanded.

This means increase or decrease in quantity demanded due to change in the price of the commodity, other factors remaining constant

It is illustrated through the movement along the same demand curve. Through extension it is increase in Qd and contraction is the decrease in Qd

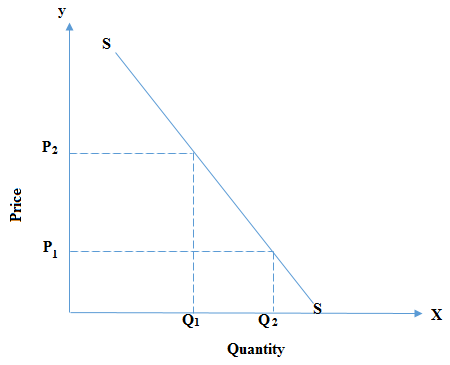

Let us assume the economy in equilibrium at point “E2” that is at price “OP2” and quantity demand is “OQ2”

Case I (contraction of demand)

Let us assume that the price increase from “OP2” to “OP1” and the quantity demand reduce from “OQ2” to OQ1”. This behavior is referred to as “Contraction of demand”

Case II (Extension of demand)

In this case the price decrease from “OP2” to “OP3” due to this the quantity demand increase from “OQ2” to “OQ3” → this is nothing but the extension of demand.

Change in demand

Is the increase or decrease in demand due to change in all the factors affecting demand apart from the price.

It is illustrated through the shift demand curve either to the right (increase in demand) or to the left (decrease in demand).

In the diagram, “dd” is original demand curve. “dd” is decrease in demand curve. “” is increase in demand curve, “OP” original price OQ – original quantity.

“OP” Original Price “OQ1” Increase in demand.

“OP” Original Price “OQ2” Increase in demand.

REASONS FOR CHANGE IN DEMAND

1. Change in the consumer’s level of income

When the consumer’s level of income increase, demand will also increase because of the increase in purchasing ability and when the level of income decrease, demand will decrease due to decrease in purchasing ability.

2. Change in population size

When the population size increases, demand will also increase because of more consumers and the population decrease demand will also decrease due to less consumers.

3. Change in the level of direct taxes

When the level of direct tax increase, demand will decrease due to the decrease of disposable personal income and when the level of direct taxes decrease, demand will increase due to the increase of disposable personal income.

4. Expectation or Anticipations

Expectations also bring about a change in demand. If prices are expected to rise in future, the demand for goods will increase now in the present. Similarly, expectation of rising incomes will restrain current purchases and post pone purchases to a future favorable situation.

5. Change in tastes, preferences and fashion.

When the tastes, preferences & fashion change in favor of certain goods, demand will increase and when the taste, preferences & fashion change against a certain good its demand will decrease.

6. Change in price of the substitute.

If the price of the substitute increases, the demand of a good in question will increase and if price of the substitute decrease the demand of a good in question will decrease.

7. Change in the price of the complement.

If the price of the complement increases, the demand of the good in question will decrease. However if the price of the complement decreases, the demand of the good in question will increase.

8. Exceptions of the law of Demand.

There are some situations where the law of demand does not operate. This gives rise to abnormal demand curve (regressive).

Aggressive demand curve has a positive slope indicating that as the price increases quantity demand also increases and vice verse. A situation which is against the law of demand.

The exceptions of the law of demand are the following;-

9. Veblen goods or Article of ostentation

These are the luxurious goods which are demand to emphasize economic status for example expensive cars, expensive mobile phones etc for such goods as the price increase, quantity demand also increases.

Giffen goods (inferior goods)

This can also be called inferior goods, example of such includes;- maize flour. For such goods when the price increases more is bought of them, but as the price fall less is demand of them for a low income earner when the price of beans increase, he will buy more of them by reducing his expenditure on meat.

Fear of the future rise in price.

When the consumers expect the price of the commodity to increase now and then because of factors such as expected shortage they will tend to buy more of the commodity as the price increases

1. Necessities

These are goods that are necessities of life, eg medicines, food, salt etc.

For such goods a minimum quantity has been purchased by the consumer irrespective of their price because of such a situation, the law of demand is operative to a certain extent.

2. Ignorance of the consumer.

These are situations where consumers buy goods at a higher price because they are ignorant of lower price for the same goods in other market.

3. Interrelated Demand

Under inter – related we examine the relationship between goods that are related in one way or another by looking at how change of one will affect demand of the other.

Types of Inter – related Demand

1. Joint Demand (complementary demand)

This is the demand for two or more commodities which are jointly needed to satisfy a particular need

Example; Car and petrol, Increase in demand of one will result into increase in demand for another and decrease in demand of one will result to the decrease in demand for another and increase in the price of one will result to the decrease in demand for another.

Price of cars

2. Competitive Demand

This refers to the demand for goods which are substitutes to one another. For example tea and coffee, Pepsi and coca cola, increase in demand for one will result into decrease in demand for another and vice verse and increase in price for one will result into the increase in demand for another and vice verse.

3. Composite Demand

This refers to demand for a commodity which can be used for several purposes e.g. demand for electricity, demand for steel.

4. Derived Demand

This refers to demand for a commodity which is used in the production of the other commodity. E.g. demand for factors of production is derived in demand because it is upon demand for goods that produces demand for factors of produce in order to produce other goods.

5. Elasticity of Demand

Definition

-Elasticity of Demand is the responsiveness of demand to change in price.

Types of Elasticity

There are basically three types of elasticity

- Price Elasticity of Demand

- Income Elasticity of Demand

- Cross Elasticity of Demand

A. Price Elasticity of Demand

Is the responsiveness of demand to change in price level. It measures responsiveness of potential buyer to change in price.

Price elasticity can be measured by the help of the following formula:

Price elasticity is always negative

Interpretation of Price Elasticity of Demand.

Perfectly in elasticity (P.E.D = 0)

This means that change in price has no effect of quantity demand.

In elasticity (P.E.D < 1)

This means that a big change in price bring about a small change in demand

Unitary (PED = 1)

This means that a change in price result into the equal change in demand

Elastic (PED > 1)

This means that a small change in price result into a big change in demand

Perfect Elastic (PED = ∞)

This means that price is not changing (fixed) but quantity demanded in changing.

FACTORS WHICH INFLUENCE PRICE ELASTICITY OF DEMAND.(PED)

PED can be elastic or inelastic depending on the following factors;-

1. Degree of availability of close substitutes

If a commodity has many close substitutes, its price elasticity of demand will be elastic as consumer can easily move over to other alternative.

However on the other side, if commodities have few substitutes its demand will be inelastic.

2. Proportion of income spent on a good

If the commodity takes a large percentage of someone’s income, its demand will be price elastic as increase in the price can easily be felt.

However if a commodity takes a small percentage of someone’s income eg. Match box its demand will be price inelastic.

3. The level of Income

With the high level of income demand will be price inelastic since increase in the price can easily be absorbed. On the other hand with the lower level of income the demand will be low hence price is inelastic.

4. Time period

In the short run demand would be price inelastic as the answer will not be able to gain enough market information e.g. the prices of other completing goods.

However in the long run demand would be price elastic as the consumer would have gain enough market information.eg. The price of substitutes.

5. The degree of necessity

If the commodity is a necessity its demand would be price inelastic as a person cannot easily do without them on the other hand, the luxurious goods have elastic demand.

6. Habit

For goods with addiction in their consumption eg. Cigarettes, alcohol, their demand is price inelastic, however those goods with no addiction use their demand is price elastic

7. Durability of a commodity.

Durable goods such as furniture have inelastic demand, since they can stand for a long period of time after has been bought on the other hand, on durable goods have elastic demand.

Importance or Practical application of P.E.D

1. To the primary decision

P.E.D is important to business in pricing decision making in order to maximize total revenue (TR). Therefore it is on the basis of the price elasticity of demand of the commodity that is selling will decide whether to increase or reduce the price (P) in order to maximize total revenue as below

When PED is perfectly inelastic he should increase the price to earn revenue since demand will remain exactly the same.

When P.E.D is inelastic, the business should decrease the price in order to earn total revenue because at such high price, demand will remain almost the same.

When price elasticity of demand is unitary the business should leave the price the same. Since increase or decrease in the price will lead to the total revenue to be the same.

When P.E.D is elastic a businessman should reduce the price in order to earn more revenue because decrease in price spark off a big increase in demand.

When carrying out price discrimination the monopolist considers the price elasticity of demand in the market in order to decide in which market to charge a high price and in which to charge low price. In that market where price is elastic, he should charge a low price and in that market where price is inelastic, he should charge a high price.

3. Wage Determination

Elasticity of demand for labor is important in wage determination in such a way that when demand for labor in a firm is inelastic, trade unions and laborers can easily succeed in bargaining for high wages than when the elasticity of demand of labor is elastic.

4. Government in Taxation

The government uses the concept of price elasticity of demand in determining which commodity to levy high tax and which to levy low taxes in order to collect more revenue. Those goods whose demand is price inelastic e.g. Cigarettes, alcohol etc.The government will levy high taxes however for the goods whose demand is price elastic the government will levy law taxes.

5. Determination of incident of a tax

Determination of the incident of a tax between producer and the buyer is on the basis of the price elasticity of demand of the commodity as below.

Demand for the commodity is price in elastic the bigger the burden is borne by the buyer and the small one by the producer.

If elasticity of demand is century the burden shared equally between the producer and the buyer.

If demand for the commodity is price elastic the smaller burden shared equally between the producer and the buyer.

If demand for the commodity is price the smaller burden is borne by the buyer and the bigger burden is borne by the producer.

6. Under International Trade (devaluation)

Devaluation is the deliberate action by the government to lower the value of its currency in relation to foreign currency. It aims at increasing export and reducing import, however this is only possible if the price elasticity of demand of both exports and imports is elastic.

B. Income Elasticity of Demand

This is the measure of degree of responsiveness of demand due to change in the consumer’s level of income.

ΔY=Changing income

ΔY=Changing incomeYo=Income before change

Q=Quantity

Interpretation of Income Elasticity.

YED = -ve

This means that a commodity is an inferior good whereby as the income increases quantity decreases

Y.E.D = +ve

This means that a commodity is a normal good therefore as the level of income increases demand increases (Articles of Ostentation)

YED = o

This means that the commodity in consideration is a necessity eg.medicine etc, therefore as the level of income increase demand remains.

YED < 1 (in elastic income elasticity)

This means that the big change in the level of income results into small change in demand. This is applicable under necessities.

YED > 1 (elastic income elasticity)

This means that the small change in the level of income results into big change in demand. This is applicable for inferior goods,

3. Cross Elasticity of Demand (CED)

This is a measure of degree of responsiveness of demand of a good due to change in price of any substitute commodity

C.E.D = Percentage change in demand for good “A”/Percentage change in price of another product “B”

Interpretation of Cross Elasticity of Demand

CED = +ve

This means the commodity in consideration is a close substitute eg, beans and peas, therefore when the price of one increase, demand of the other increase and vice versa.

CED = -ve

This means that two commodities in consideration are complement (jointly demanded) e.g. car and petrol for such goods when the price of one increases demand for the other decrease and vice versa.

CED = 0

This means that the two commodities in consideration are not related at all, therefore a change in the price of one does not bring about any change in demand of the other e.g. Car and table

Arc and Point Elasticity.

Arc Elasticity

According to Baum, “Arc Elasticity is a measure of the average responsiveness to price change exhibited by a demand curve over some finite stretch of the curve”

Or

Arc elasticity is an estimate of the elasticity along average of demand curve. It can be calculated for both linear and non linear demand curve using the following formula.

Point Elasticity

Point Elasticity of demand is measured by the slope of tangent to the demand curve at that point.

Price elasticity with complete accuracy at a point on the demand curve.

The formula for calculating point elasticity of demand is as follows;-

Point ed = -Dq/q

Dp/p

= Dq x Po

Dp qo

Factors of Elasticity of Demand

There are several factors which determine the elasticity of demand.

These are the following:-

For necessaries of life demand is less elastic.

As regards the necessaries of life demand is less elastic because these commodities are purchased at whatever price they may be. They change in price does not matter so far as demand for such commodities is concerned. Wheat and cloth are examples of such things.

Demand for luxuries is more elastic.

The demand for luxuries is more elastic in the sense that a little change in price level brings a greater change in demand. Television and video sets are examples of such things

For substitute demand is more elastic.

The commodities which have their substitute, their demand is more elastic. For example, when price of tea rises, demand for tea will decrease to great extent because more coffee will be demanded.

Demand for goods having several uses is more elastic.

The commodities which have various uses, they have more elastic demand. Coal is such a case when it is cheap the use for less urgent needs will extend and when its price goes to rise, it will be put only to more urgent uses and its demand will decrease to a great extent.

Demand for goods the use of which can be postponed.

Demand for goods, the use of which can be postponed is more elastic ‘for example, when building material is very costly, the building activities are very much reduced and vice versa.

Price level

Elasticity also depends upon the price. If the price is either too high or too low, the demand will be less elastic. For example, in the case of cars and salt.

THEORY OF SUPPLY

Supply means the quantity of goods services a producer is willing and able to offer for sale in the market at the prevailing price per period of time.

The law of supply states that, “The higher the price the higher the supply and the lower the price, the lower the supply, other factors remaining constant.

Assumptions of the law of supply.

The law of supply operates all factors affecting supply are kept constant apart from the price therefore the following gave its assumptions.

<> The level of technology is constant

<> The climatic season remains the same

<> The number of producers remains the same

<> The government policy remains unchanged.

<> The price factor of inputs remains fixed

<> The level of demand remains the same

<> The prices of other related goods remains the same.

Supply schedule

Is a table that shows various quantities of goods and services offered for sale are their corresponding prices.

An individual supply

Is a table that shows various quantities of goods services a single producer is willing and able to offer for sale in the market at different prices per period of time.

Market supply schedule

Is a table that shows different total quantities that producers are willing and able to offer for sale in the market at different prices per period of time.

Note: In order to get a market supply schedule we add up individual supply schedules

Supply curve

Is a geometrical representation of various quantities offered for sale by producer of a commodity and their corresponding prices.

Note: The supply curve can be an individual or market supply curve, therefore in order to get a market supply curve we add up individual supply curves.

Factors Affecting Supply

1. Price of the commodity

The higher the price of the commodity, the higher the supply,the lower the price of the commodity, the lower the supply, other factors remaining constant.

2. Number of producers.

If there is a big number of producers of a particular commodity, supply will be high and when there is less number of producers of a particular commodity supply will be low.

3. Production technique (level of production)

With the use of improved and better technology, supply will be big. However the use of inferior and low level of technology, supply will be low.

4. Government policy

Provision of subsides to producers results into more supply as it lowers the cost of production on the other hand imposition of taxes discourages producers and hence low supply.

5. Gestation Period ( production period)

The shorter the gestation period, the higher the supply and the longer the gestation period, the lower the supply.

Time in the short run, supply will be less since some factors input will be fixed. However in the long run supply will be high as the form will be able to very all its factor in put

6. Price of the substitutes

When the price of the substitute is high, supply of a good in question will be low because of low level of profitability but however the price of the substitute is low supply of a good in question will be high.

Price of the complement (Jointly Supplied goods)

When the price of the complement is high, supply of a good in question will be high and the opposite is true. E.g. when the price of meat is high supply of hides will also be high and vice versa

Change in Quantity supplied and change in supply

This means increase and decrease in quantity supplied due to change in the price of the commodity other factors remaining constant.

When the price increases quantity supplied increase and with the price decrease quantity supplied decrease.

Change in supply (Rise and Fall in Supply)

Change in supply (Rise and Fall in Supply)

Also referred to the shift of the supply curve. This means rise or fall in supply due to all factors affecting supply apart from the price. When the supply curve shifts to the right it means a rise in supply and when it shifts to the left it means decrease/ fall in supply.

FACTORS OF CHANGE IN SUPPLY

1. Cost of Production.

When cost of production of any commodity rises, supply falls and vice verse.

2. Climate situation

If climatic situation remains favorable agricultural production will increase and as a result of this supply will rise and vice verse.

3. Improvement in the method of production.

When new and less expensive methods of production are invented, supply will increase/ rise and vice verse.

4. Development of means of transport and communication

If means of transport and communication are adequate and developed, it will be possible to move commodities from one place to another place. In this case supply will rise and vice verse.

5. Peace and security.

With peace and security, supply rises because production is encouraged and vice verse

6. Policy of the Government.

When restrictions are levied by the government on the movement of goods, supply will fall and when such restrictions are removed supply will rise.

7. Rates of Taxes

When taxes are levied at a higher rate, supply falls and vice verse.

8. Abnormal Supply curve

Is that supply curve which disobeys the law of supply. It has a negative slope. It implies that the higher the price of the commodity, the lower the quantity supplied of it and vice verse.

The cases of abnormal supply curve are not common. In very rare cases only a supply curve will be of the abnormal shape. There is one good example of abnormal supply curve i.e. the bending supply curve of labor.

This shows that beyond a specific wage level, any rise in ways will result in decrease in working hours. The shape of the supply curve of labor is as under.

When wages rise beyond OW then working hours decrease.

Inter – related supply

1. Joint Supply

Some goods are produced together. The supply of those goods which have common process of production is known as joint supply. The supply of such goods is increased or decreased simultaneously.

E.g. a) Wood and Mutton are produced jointly

b) From crude oil, different types of petrol production are obtained

Such as diesel, engine oil, super etc.

2. Composite Supply

The goods which are substitute of one another their total quantity is called composite supply.

E.g. a) Supply of Mutton, beef and chicken

b) Supply of Tea and Coffee

c) Supply of cold drinks like Coca cola and Pepsi

3. Competitive Supply.

There are some alternative uses of land, labor and capital. If these factors are used for the production of one commodity then the supply other commodities is affected.

E.g. a) If more land is used to produce wheat then production of maize will

Decrease. The supply of these goods is competitive supply

ELASTICITY OF SUPPLY.

Elasticity of Supply – Is the measure of the ease with which an industry can be expanded and of the behaviour of the marginal costs.

A. Price Elasticity of Supply

Price elasticity of supply is the measure of degree of responsiveness of supply due to change in price of commodity

P.E.S = (proportional change in amount supplied)/(proportional change in price)

Interpretation of PES

PES = 0 (perfectly inelastic)

This means there is no change in quantity supplied due to change in price

PES < 1 ( inelastic )

This means that the change in price is greater than the change in quantity supplied

PES = 1 (unitary)

This means the amount of change in price is equal to the amount of change in quantity supplied

PES > 1 (elastic)

This means that change in quantity supplied is more than change in price.

PES α (perfectly elastic.)

This means that there is no change in price but there is change in quantity supplied

FACTORS THAT INFLUENCE P.E.S.

1. Gestation Period.

If a commodity has a short gestation period its supply will be price elastic as supply can easily be increased in a shorter period of time. E.g. industrial goods, however if a commodity has a longer gestation period its supply will be price in elastic eg. agricultural goods.

2. Degree of entry of new firms in the market.

If there is free entry of firms in the market eg. under perfect competition supply would be price elastic. However if there are barriers to entry of new firms in the market. E.g. under monopoly supply would be price inelastic.

3. Ability to store stock

For those commodities which can easily be stored their supply is price elastic, as supply can easily be increased from the existing stock. However for those goods that can easily be stored e.g. vegetables, their supply is price in elastic.

4. The existence of spare capacity

If a firm is operating at full capacity, further increase in output will be more difficult and hence in elastic supply. However if a firm is operating below full capacity supply will be price elastic as more output can be product by further utilizing, the underutilized factor inputs.

5. Time

In the short run supply would be price inelastic as some factors input will be fixed e.g. land, capital, and technology. However in the long run supply it will be elastic as all factor inputs will be variable.

6. The level of technology

With the use of advanced technology, supply will be price elastic as such technology is more efficiency. However with the case of poor technology supply will be inelastic as such technology is less efficient.

7. Cost and availability of factors of production.

When the cost of production is low and there is adequate supply of factors of productions, supply will be price elastic. On the other hand when the cost of production is high and there is limited supply of factors of production, supply will be inelastic.

8. Cross Elasticity of Supply

It is the proportional (percentage) change in the supply for good x divided by the proportional (percentage) change in the price of good y

CES = +ve

This means that the commodity in consideration are complements (jointly supplied) e.g., meat & hides. When the price one increase, quantity supplied of the other also increases and vice versa

CES = -ve

This means that the commodities in consideration are substitutes e.g. beans & peas, when the price of one increase, quantity supplied of the other decrease and vice versa.

CES = 0

This means that the commodities in consideration are not related at all, therefore change in price one cause no effect in quantity supplied of the other e.g. a car and a table.

Factors of Elasticity of Supply

1. Nature of commodity

Those commodities which are durable can be kept for a long time and such commodities like wheat and cloth have a greater elasticity of supply. The commodities which are perishable nature like fish and milk have less elastic supply.

2. Costs of Production.

The commodities which have high costs of production have less elastic supply and vice versa.

Those commodities which are produced in a short period of time have greater elasticity and vice versa.

3. Methods of production.

The commodities which can be produced with the help of simple methods of production have more elasticity and if the method of production is complicated, supply will be less elastic.

4. Laws of Returns.

The commodities which are produced under the conditions of increasing returns have greater elasticity of supply and the commodities which are produced under the condition of diminishing returns have smaller elasticity of supply.

5. The equilibrium between Demand and Supply

This is when quantity demanded is equal to quantity supplied, therefore there is neither shortage nor surplus. When the demand and supply curve meet at that particular point, qty dd is equal to qty ss.

The point of intersection is the equilibrium point, consisting of the equilibrium quantity and price,.

| Px | Dx | Sx |

| 1 | 500 | 100 |

| 2 | 400 | 200 |

| 3 | 300 | 300 |

| 4 | 200 | 400 |

| 5 | 100 | 500 |

Price 3 is the equilibrium price and quantity 300 is the equilibrium quantity

The price above the equilibrium price supply increases but demand decreases and hence a surplus

The price below the equilibrium price, supply decreases but demand increases and hence a shortage.

The effect of changes in demand of equilibrium point, price and quantity

The effect of change in supply of equilibrium point, price & quantity.

Demand and supply functions

The demand function is a mathematical relationship between demand and factors that determine demand.

Qd = f (P x, TP, Y, Pr, ………….)

Whereby,

Px = Price of the commodity

TP = Taste and preference

Y = Income level of consumers

Pr = Price of related goods.

Since price is the major factor that affects demand, the demand function can as well be shown using the price quantity relationship as below;-

Qd = f(P)

The supply function is a mathematical relationship between supply and the determination of supply.

QS = f (P x, T, NP, Pr, GP, ……………)

Whereby,

P x = Price of the commodity

T= Time

NP = Number of Producer

Pr = Price related commodities

GP = Gestation Period

Since price is the major factor that affects supply, the supply function can as well be given as

Qns = f(P)

WAYS OF PRICE DETERMINATION

1. Price mechanism

Under this, the price of the market is determined by the free interaction of the forces of demand and supply and hence determined at the point where the demand and supply curve intersect or meet.

2. Sale Auction

The price is determined through bidding; therefore it is determined by the highest bidder

3. Haggling

This is through bargaining.

Re sale price mechanism.

Under this the price of the product is determined by the producer.

The price can as well be determined by the government and this can either be a maximum or minimum price.

Price ceiling (maximum price) is the price which is set by the government below the equilibrium price, this is normally done during the period of shortage, when price of essential goods are excessively high. Therefore it aims at protecting consumers against such excessively high price.

Effects of Price ceiling

Demand will increase (to ) hence a shortage (Q1-Q2)

Supply will decrease ( to

Black market – sellers are going to sell products in order to create an artificial shortage

Corruption & far nism- they will sell the product to those who are willing to buy.

Advantages of price ceiling

It helps to control inflation.

It reduces exploitation on the consumers.

It allows consumers to easily access essential goods at affordable prices during periods of shortage.

It helps the government to win more support.

Disadvantages of Price Ceiling

Discourages producers.

It is expensive to administer.

It creates black market

Minimum Price ( Price Floor)

This is the price which is set by the government above the equilibrium price. It aims at motivating producers after realizing that, the prevailing market price is low.

Effects of Price Floor

Supply increases from to

Demand decreases from to

Sellers will be tempted to decrease price in order to get rid of surplus.

It helps to improve the standard of living of workers.

Disadvantages of Price Floor

Over production

It results into cost-push inflation.

It can cause unemployment.

In case of minimum wage discourages investments.